The Perch: January Issue

Dr.V, Ian Chang

The AI Question

Last year, the million-dollar question for investors was when AI companies would generate real revenue. That question has now been decisively answered: at least 20 AI companies generate $100M+ in recurring revenue, excluding incumbents such as Anthropic and OpenAI.

In 2026, the question has shifted. Investors are no longer asking whether revenue exists, but whether meaningful margins can be achieved.

We believe there is; the technology will mature, inference will become more efficient, and ongoing research will improve models without scaling compute.

So, are we in a bubble?

It’s hard to give a definitive answer. The market is likely both under- and over-valuing high-priced assets. Investors are underwriting sharply different views on research (e.g., the possibility of an AGI breakthrough), adoption (e.g., agent performance and attention spans), addressable market (e.g., will U.S. companies be allowed to operate in the EU long term?), and who ultimately wins (e.g., a major investor has invested in both Abridge, the disruptor, and Epic Systems, the incumbent).

For us, at the first-check stage, long-term performance is largely unaffected by short-term market bubbles. There is a low likelihood that AI research will plateau, and there remains significant headroom in adjacent markets such as robotics. As a result, we remain optimistic and continue to push forward with conviction.

At the same time, out of caution, we are encouraging portfolio founders who had planned to raise in H2 ‘26 or later to revisit their timelines and consider raising now.

Fund Update

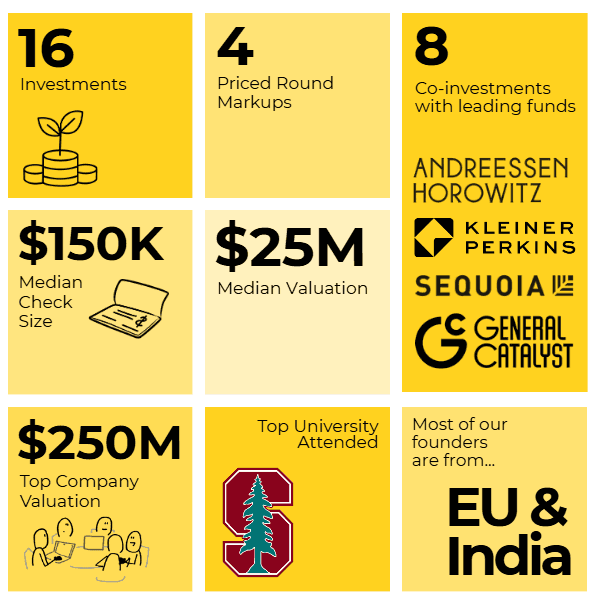

By the New Year, we have deployed $1.9M across 16 portfolio companies, with 10 receiving $150K+ in capital. Our median entry valuation is approximately $25M, and our median check size is $150K.

Anterior is now our highest-valued portfolio company at approximately $250M, while our founder base is growing increasingly global, with a majority born in the EU and India.

In terms of co-investment, General Catalyst has been our most frequent partner (three deals), followed by Kleiner Perkins, Sequoia, NEA, Accel, and Lightspeed, each participating in one deal.

Lessons Learned in 2025

Single-winner fallacy: The last SaaS era trained investors to ask, “Who is most likely to win this category?” Our key realization has been that there will be many winners across sub-niches within the same category, because:

A technical disruption dislocates incumbents across all markets simultaneously, creating multiple parallel opportunities. This dynamic differs from mature markets, where each new opportunity typically requires a hard-won, idiosyncratic insight to build a valuable business.

A “single market” is often the sum of many rich sub-markets. We now think of legal AI not as one monolithic market, but as a portfolio of distinct segments—for example: workforce automation for plaintiff firms (Eve, valued at $1B+), demand-letter automation for personal injury lawyers (EvenUp, valued at $2B+), and general-purpose AI paralegals (Harvey, valued at $5B+).

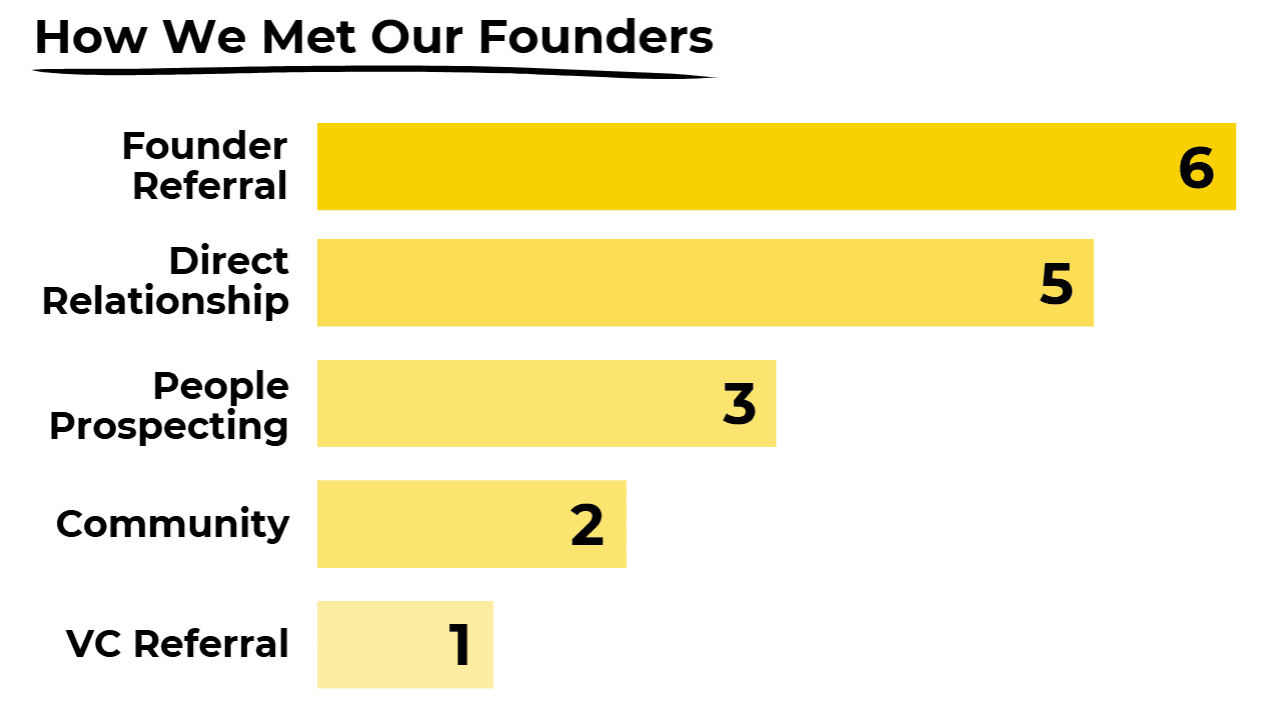

Speed is a meaningful edge in venture. In a market where founders frequently complain about firms ghosting them, we routinely make decisions within under 2 days—while still conducting rigorous diligence. A pre-existing founder network, prepared points of view, and a small team drive our velocity. We’re also actively exploring how AI can further accelerate our decision-making.

Financing has emerged as our most frequently cited right to win. Founders consistently highlight our disciplined milestone planning for Series A and the candid backchannel feedback we provide after investor meetings—support they say is difficult to find elsewhere.

European founders have surprised us with both their quality and volume. While the conventional wisdom is that “the best European founders are already in the U.S.,” roughly half of our founders were previously based in London before relocating and starting anew. India has been the second-largest source of portfolio founders.

Founder quality > valuation discipline. We’ve learned that we have limited influence over entry valuations for top-tier founders, mainly due to structural market dynamics. At the same time, AI companies have reset valuation benchmarks significantly higher.

As a result, at the margin, we prioritize founder quality over strict valuation discipline—without going overboard. Looking ahead, the ability to write larger checks (~$1M) in subsequent funds will give us greater pricing power and leverage on entry.

Latest Investment

Recently, we invested in Perpetual, a next-generation wealth management platform bringing Iconiq-level service to mass-affluent clients. The round was led by Accel Partners, alongside our participation.

Perpetual acquires anchor RIAs, centralizes data ingestion, compliance, and marketing through AI, and expands access to differentiated alternative investment products.

We found this investment compelling because:

Wealth management is a large, fragmented, and growing market: The U.S. holds approximately $168.8T in household wealth, with 22,000+ SEC-registered RIAs managing $85T+ in investable assets. Despite this scale, the market remains highly fragmented — ~85% of RIA firms manage under $500M in AUM. Independent RIAs have gained 11 percentage points in market share from 2014 to 2024 as wirehouses have retreated. Additionally, an estimated $61T in wealth is expected to change hands through generational transfer. At roughly $100T in addressable AUM, we estimate this represents a $7–10B market opportunity.

Repeat, top-quality founder: Shashank previously co-founded and led CasaOne, a furniture and outdoor rental marketplace, demonstrating a strong ability to operate at scale, raise debt capital (e.g., $50M+ from Credit Suisse), and win competitive, high-stakes deals.

Changing investor preferences: Investor demand is shifting toward crypto, venture capital, private equity, and real estate — products that most independent RIAs do not currently offer. At the same time, over 50% of firms report losing clients due to poor digital experiences, creating a meaningful opportunity for modern, tech-enabled platforms.

Proven AI efficiency: AI can reduce the back-office workload by 30–70% while increasing the client-to-advisor ratio. Many components of wealth advisory resemble customer support and compliance workflows, both of which have seen significant efficiency gains over the past year through automation.

Quality syndicate: RIA roll-ups require meaningful upfront capital, making it critical that Accel led a $15M large-seed round. This strategy is increasingly validated by participation from non-traditional investors such as General Catalyst and Thrive, signaling broader institutional confidence in the model.

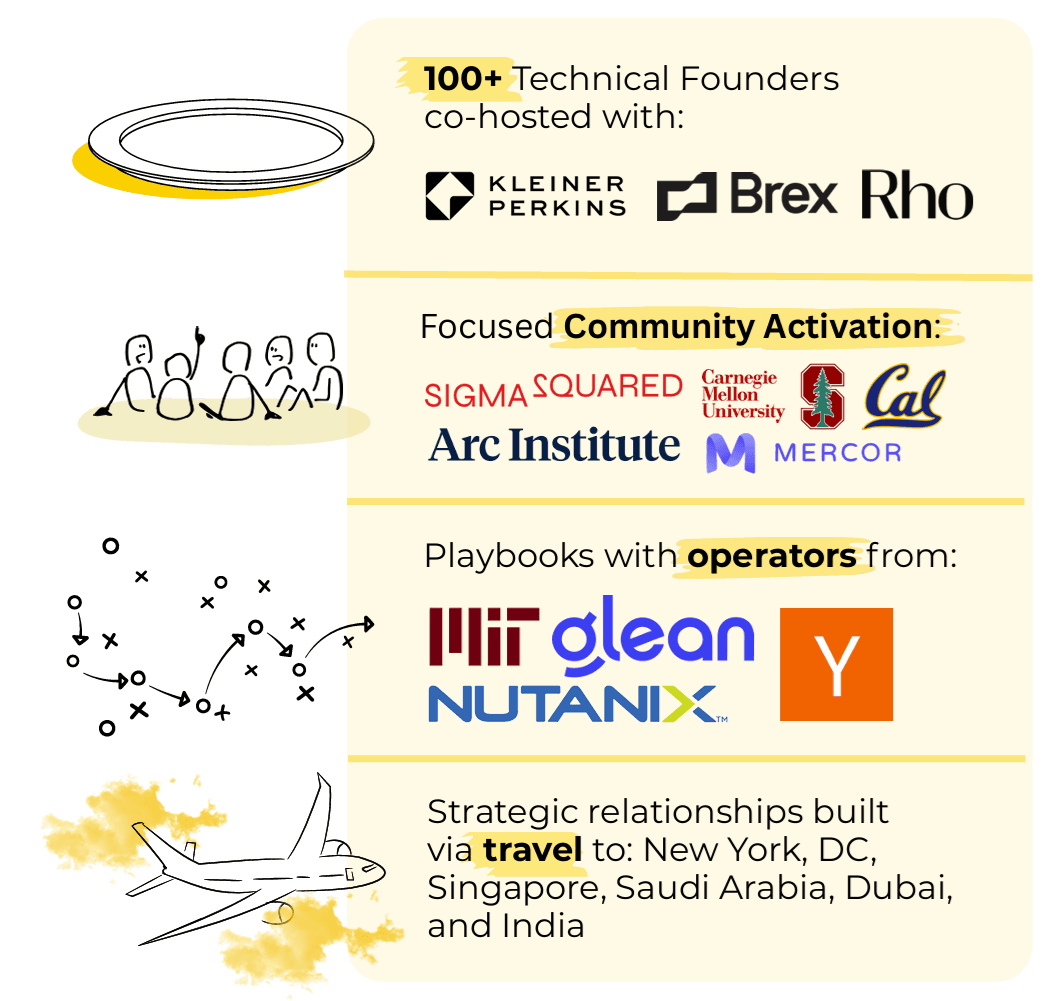

Community

2025 was a year of rapid experimentation. We hosted dinners with high-signal founder communities, co-ran technical builder events with top venture firms, recorded podcasts with strong operators and founders, and showed up consistently at ecosystem events. As a result, we sourced two deals and built a more visible and trusted presence in the market.

Future Plans

The AI opportunity is among the largest we’ve seen, and it’s rapidly growing, so we will continue to meet with leading founders in this space early, often before other firms. Buying ownership early by writing larger checks is simply good business!

We’ve also begun receiving inbound interest from institutions for our next fund, and we’re grateful that nearly all current LPs have expressed an appetite to write larger checks. At the same time, we see a clear opportunity to add high-quality talent to strengthen our team.

So we’re taking the same advice we give our companies: raise sooner rather than later. Same strategy, a sub-$50M fund, ~$750K–$1M checks… more to come in the coming weeks.

We wish you a fantastic year,

Team ODDBIRD